Understanding Consumer Financial Trends and How They Shape Home Improvement Decisions

Today’s home improvement market is increasingly shaped by consumer financial trends like savings, debt, inflation, and confidence. For contractors, this creates a critical shift: Success today depends not only on delivering strong estimates and quality work—it’s about understanding how and why homeowners make financial decisions.

It’s essential that contractors today understand the key consumer financial trends influencing homeowner behavior and how those trends directly impact your ability to close jobs, maintain margins, and grow your business.

In this guide:

Why Consumer Financial Trends Matter for Home Improvement Contractors

Today’s home improvement market is shaped as much by consumer confidence and household budget pressure as it is by demand. The total home improvement products market is projected to reach about $688 billion by 2029 (HIRI)—yet individual homeowners are still feeling squeezed.

Across the industry, contractors are already seeing:

- Longer sales cycles as homeowners deliberate more carefully

- Increased price hesitation even on essential repairs

- Higher demand for payment flexibility and monthly payment options

Understanding consumer financial trends is critical for strategic sales and margin protection. Contractors who ignore these shifts risk losing bids to competitors who have adapted.

The Financial Reality Shaping Homeowner Decision-Making

Homeowners are financially constrained by limited savings, rising costs, and high debt, which directly impacts their ability to move forward with projects.

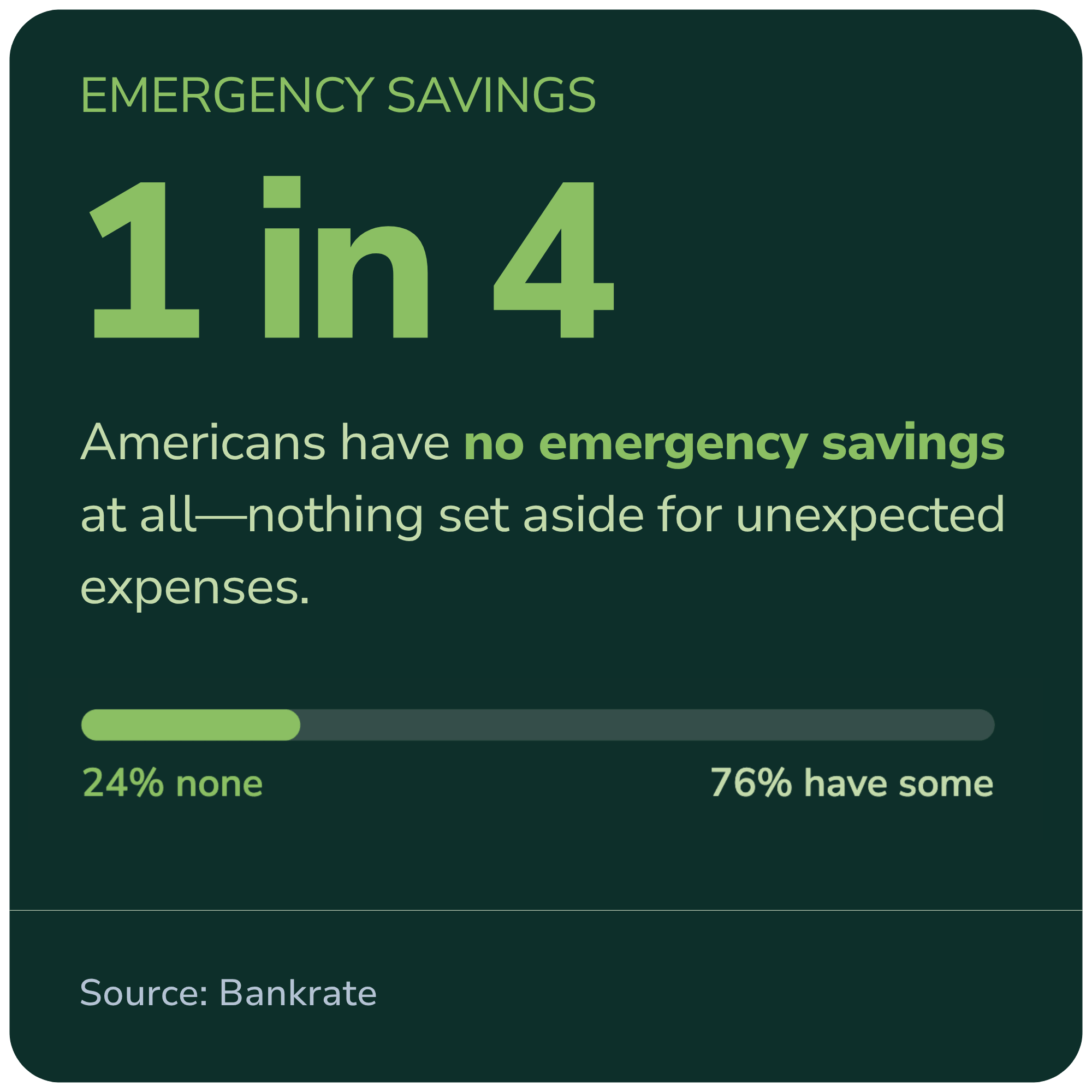

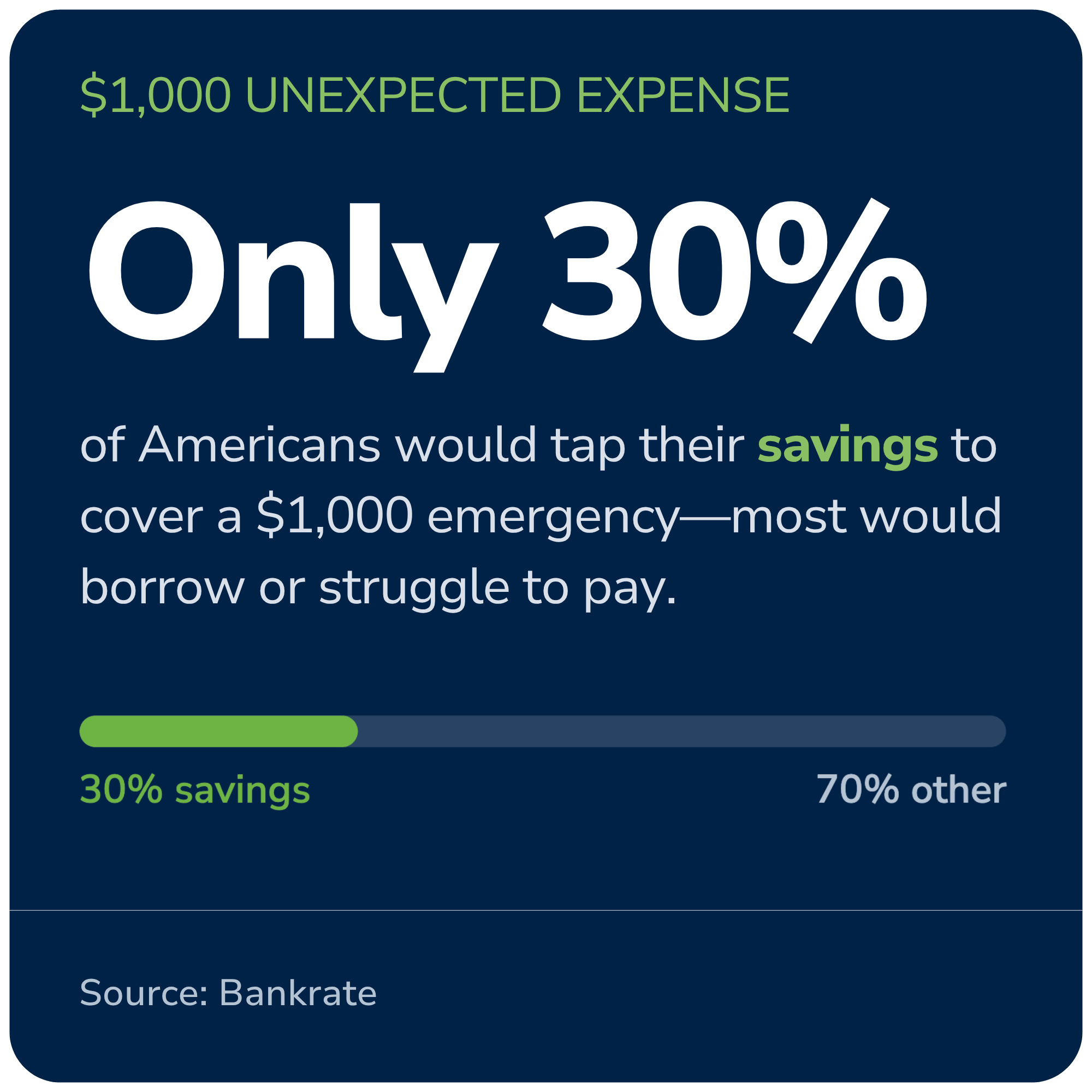

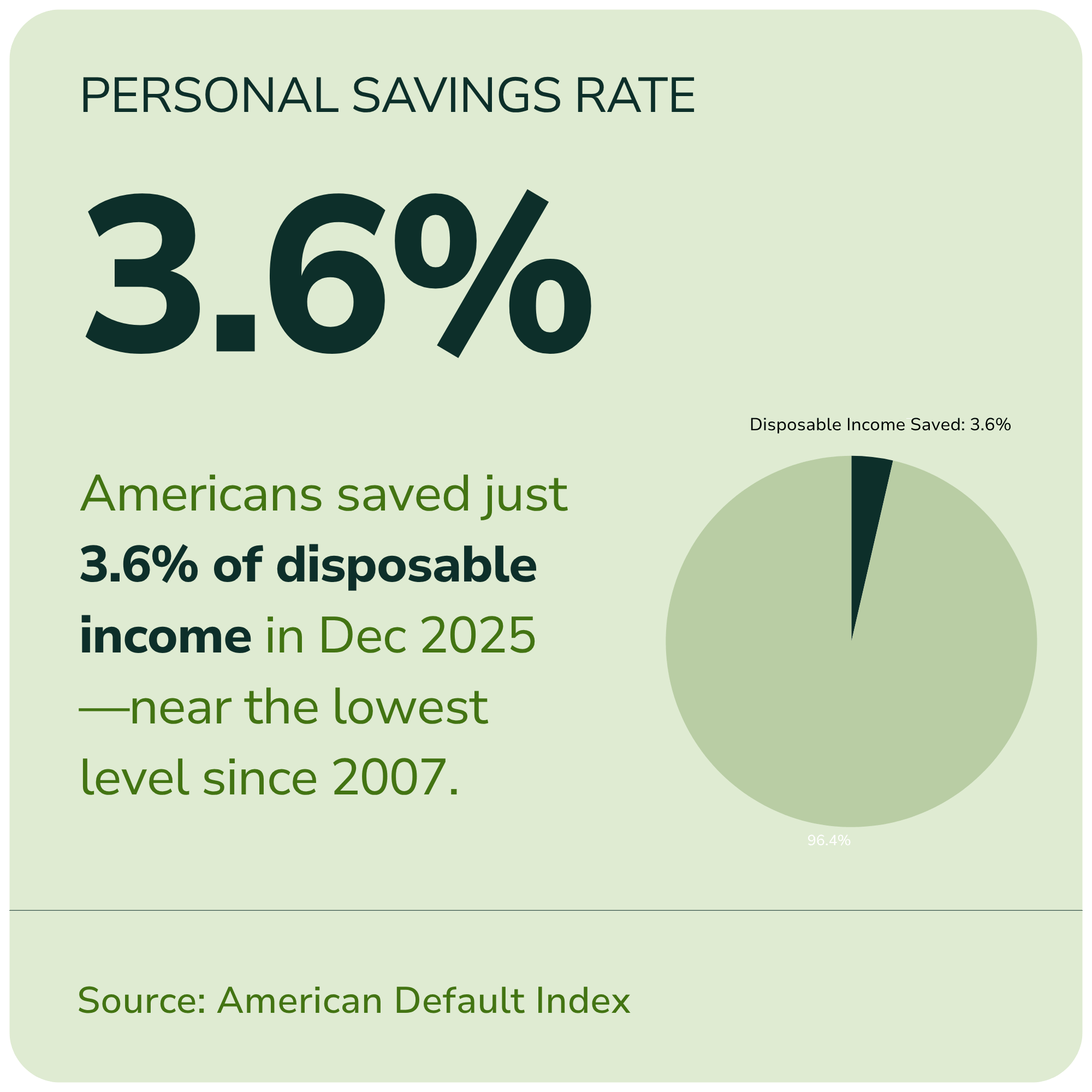

Limited Emergency Savings

Many homeowners lack sufficient savings for unexpected repairs—which means even urgent projects can feel unaffordable:

- Nearly 1 in 4 (24%) of Americans have no emergency savings at all (Bankrate)

- Just 30% of Americans would use their savings to pay for a $1,000 major unexpected expense (Bankrate)

- Americans saved just 3.6% of disposable personal income in December 2025, near the lowest level since 2007 (American Default Index, "The Buffer")

Emergency projects (e.g., a failed HVAC system, a leaking roof, a broken water heater) often collide directly with limited cash availability, creating pause at the exact point when homeowners need to act fast.

Rising Cost of Living Pressures

Wage growth has consistently failed to keep pace with rising costs across essential categories — housing, utilities, food, insurance, and energy — leaving less room in household budgets for anything beyond necessities.

- The average American paycheck has failed to keep pace with the rising cost of essential services, including housing, childcare, and medical expenses (Prosperous America)

As a result, home improvement projects are increasingly viewed as discretionary — or “stretch” — expenses, even when homeowners genuinely want to move forward.

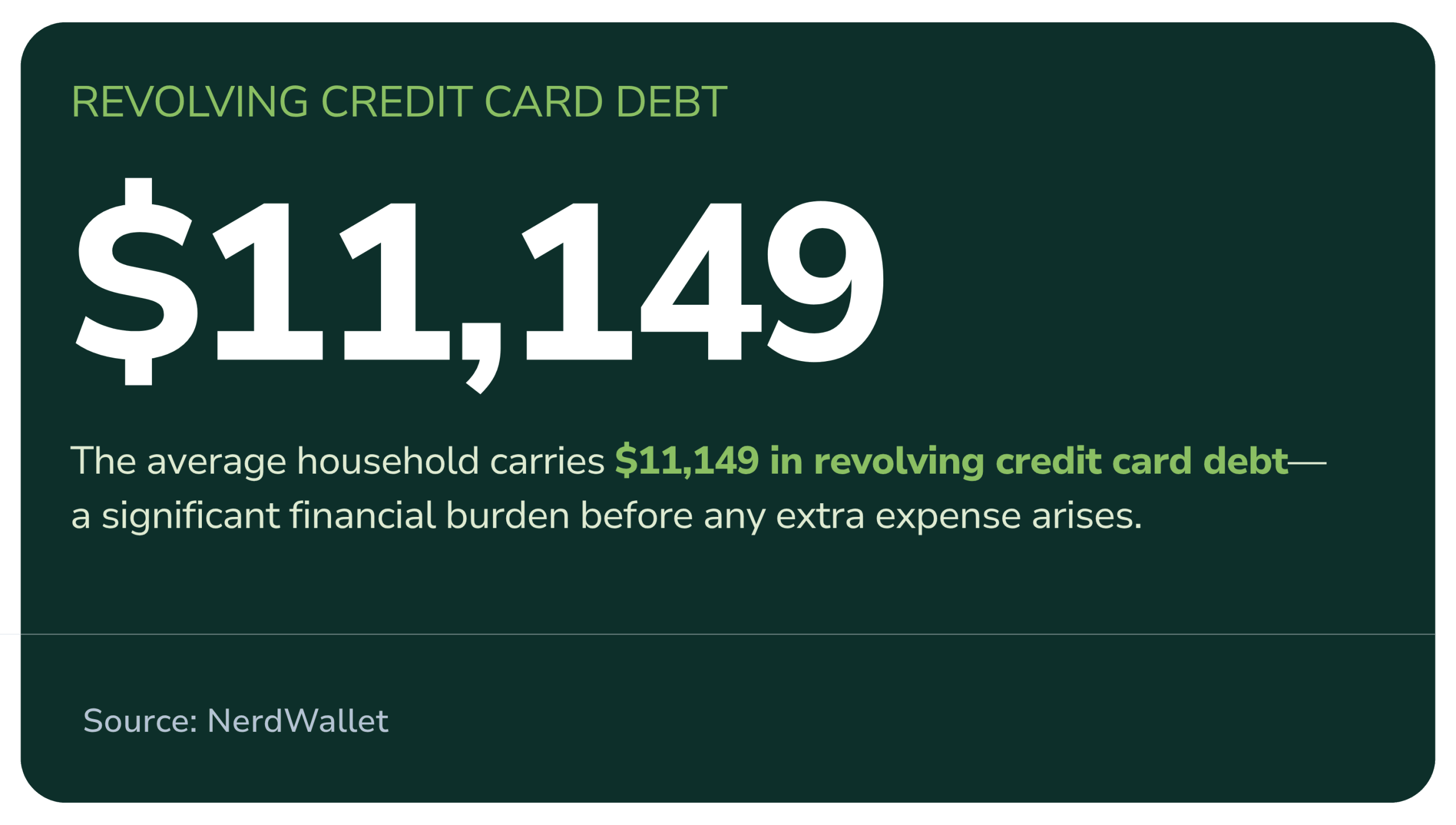

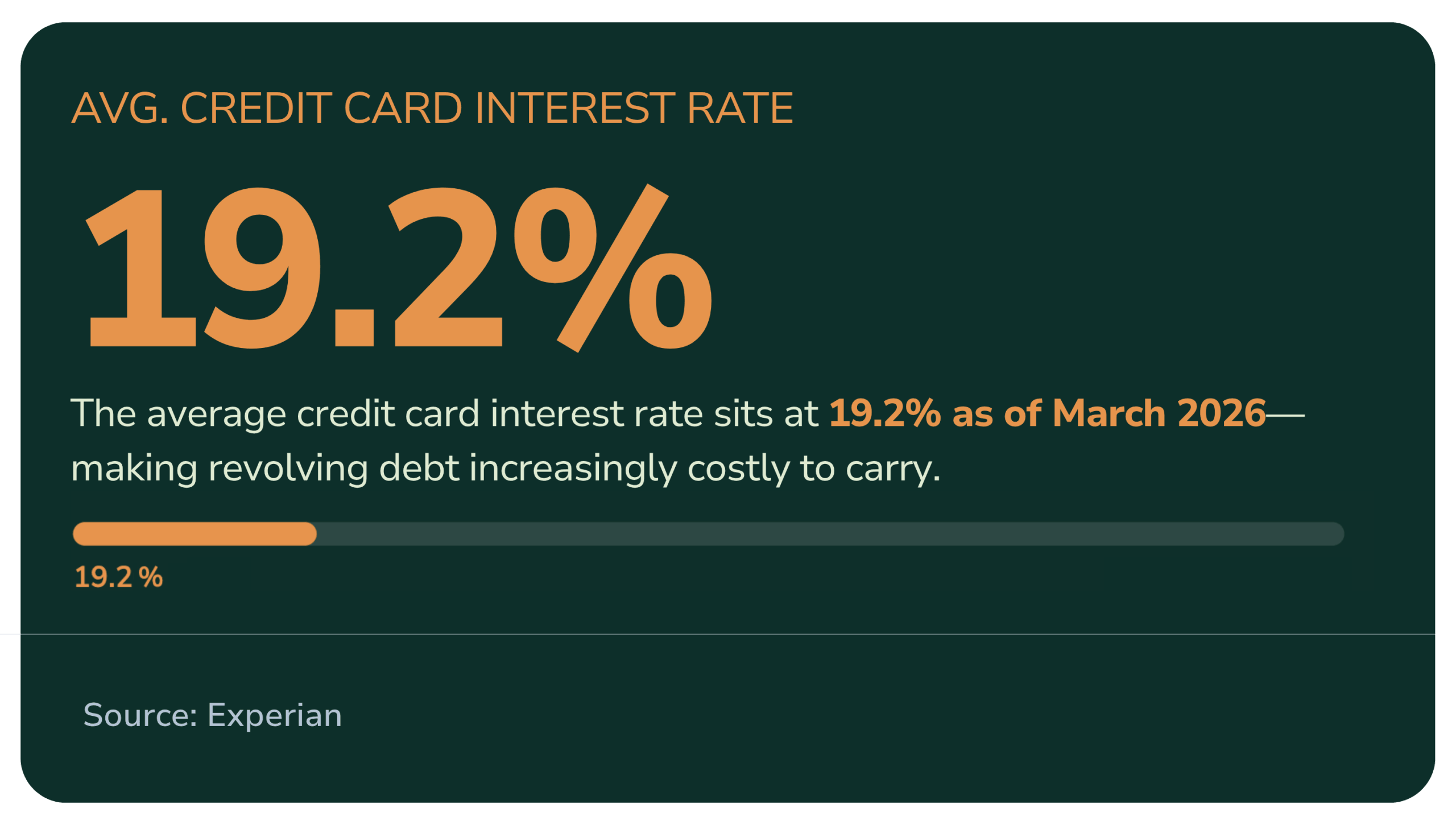

Growing Reliance on Credit Cards

With limited savings and rising expenses, many homeowners turn to credit cards to fund home improvement projects, but that option has limits too.

- The average household carries $11,149 in revolving credit card debt (NerdWallet)

- High balances mean many homeowners are already near their credit limits before a project even starts

- The current credit card interest rate averages 19.2% as of March 2026 (Experian)

📋 Contractor takeaway: Homeowners may want to move forward, but financial constraints—limited savings, rising expenses, and capped credit—often dictate when and how projects actually happen.

Willingness to Spend vs. Ability to Pay in Home Improvement Spending

A key dynamic in today’s market is the growing gap between willingness and ability.

| Term | What it means | Trend we’re seeing |

|---|---|---|

| Willingness to spend | The homeowner wants to pay for a project (desire, motivation, prioritization) | Steady but cautious — Most homeowners are prioritizing home improvement over other discretionary spending (HIRI) |

| Ability to pay | The homeowner can pay for a project without financial strain (cash, savings, credit) | Declining — limited emergency savings, rising costs of living, and credit limits constrain capacity |

Even motivated homeowners may not have the financial capacity to move forward without strain. This disconnect is reshaping home improvement spending across the industry.

This gap often leads to:

- Delayed projects—homeowners who intend to move forward but keep postponing

- Reduced project scope —choosing the minimum viable fix rather than the ideal solution

- Sticker shock during estimates—even when the price is fair and competitive

Shift Toward Monthly Payment Thinking

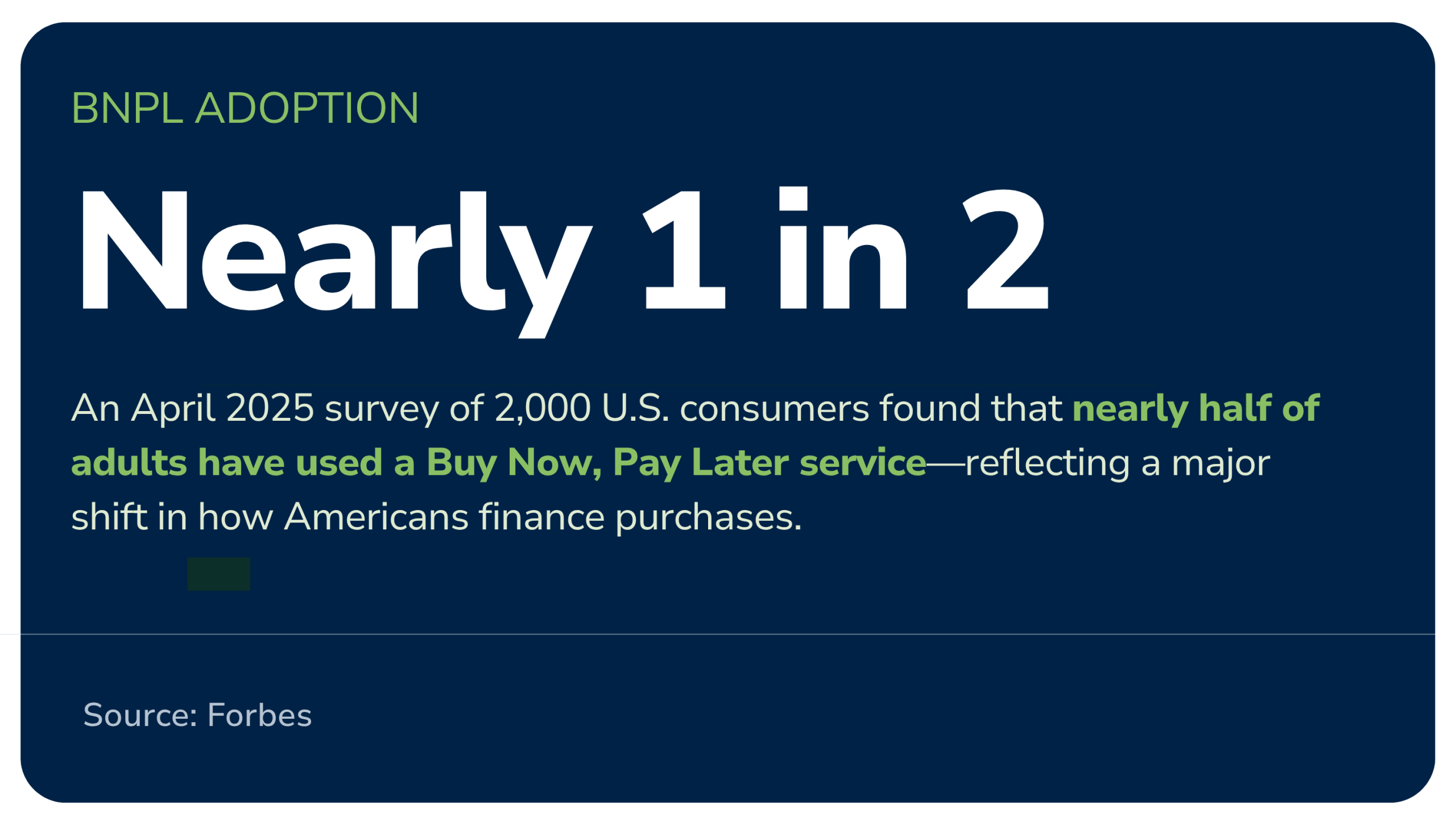

Homeowners are increasingly thinking in terms of flexible payment options rather than total project price. Buy-Now, Pay-Later options are now being used even for smaller everyday purchases, highlighting a broader trend: many consumers in the home improvement space also need or prefer flexible payment solutions.

- An April 2025 survey of 2,000 U.S. consumers aged 18 to 79 found that nearly half of adults have used a BNPL service (Forbes).

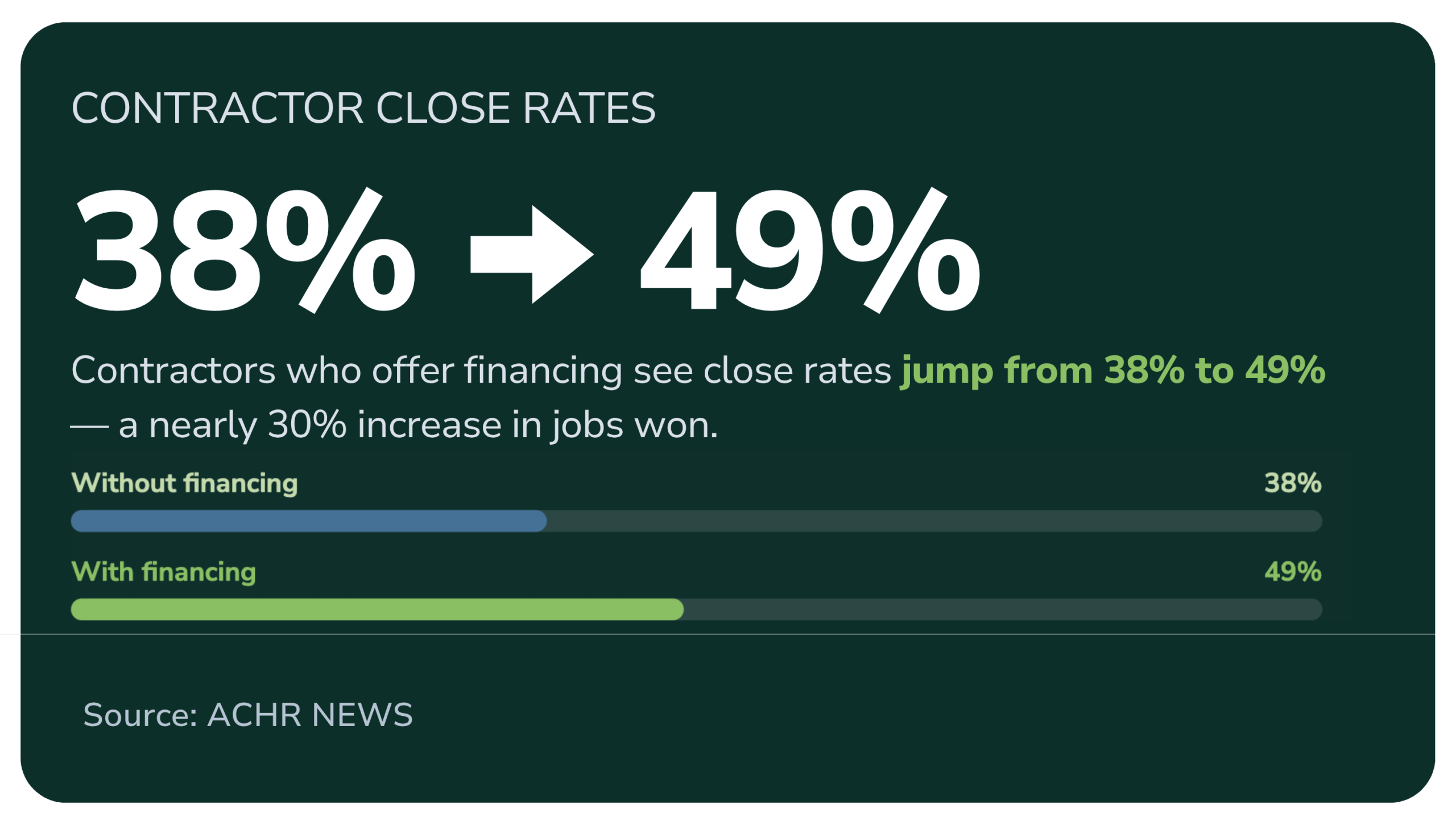

- Contractors who offer financing see close rates jump from 38% to 49% (ACHR News)

The contractors who understand this shift aren’t just closing more jobs. They’re removing the single biggest barrier standing between a motivated homeowner and their ideal home project.

Consumer Confidence, Future Savings, and Buying Hesitation

Homeowner hesitation is not driven by price alone. In today’s market, it is more often the result of broader uncertainty around financial stability, future income, and overall consumer confidence.

This uncertainty is reflected across multiple economic indicators:

- The Consumer Confidence Index (CCI) declined by more than 18% between December 2024 and December 2025 (HIRI)

- 52% of workers expect nationwide layoffs to increase in 2026, signaling growing concern about job security (Monster)

- 58% say their biggest concern for 2026 is that their salary will not keep pace with inflation, reinforcing ongoing financial pressure (Monster)

Taken together, these signals point to a consumer base that is increasingly cautious—not necessarily unwilling to spend, but more deliberate in how and when they commit to major expenses like home improvement projects.

This hesitation often appears in the sales process in predictable ways:

- Delayed approvals after receiving an estimate

- Requests for multiple bids without a clear decision

- “We’re going to wait” responses without a defined timeline

In many cases, the homeowner still wants to take on home improvement spending. However, uncertainty about job security, income stability, or broader economic conditions causes them to pause and reassess timing rather than immediately commit.

💡 Key insight for contractors: Hesitation is rarely just a reflection of price sensitivity. It is more often a form of risk management. Contractors who recognize this dynamic are better equipped to respond with empathy, reduce friction in the decision-making process, and guide homeowners toward a level of comfort that allows the project to move forward.

How Inflation and Rising Costs Affect Home Improvement Decisions

Inflation has increased the cost of goods, services, and energy across the economy, with consumer prices rising 2.7% year-over-year as of December 2025, continuing to put pressure on household budgets (U.S. Bureau of Labor Statistics, Consumer Price Index).

For homeowners, rising energy prices are influencing demand for:

- Full HVAC replacements

- Energy-efficient upgrades

- Preventative maintenance

Homeowners are increasingly weighing:

- Short-term affordability

- Long-term operating cost savings

📋 Contractor takeaway: Rising costs may delay decisions, but motivated homeowners can still want to invest when they can envision long-term value. Contractors who understand these pressures can guide more productive conversations—focusing on long-term ROI, energy savings, and preventative cost avoidance.

Generational Differences in Home Improvement Spending

Homeowner behavior varies significantly by life stage, and a sales approach that resonates with one generation may fall flat with another. Understanding generational differences allows contractors to tailor their conversations more effectively from the first estimate.

Younger Homeowners

- Limited cash reserves: Younger homeowners are often earlier in their financial journey, balancing student loan obligations, rising housing costs, and fewer years of accumulated savings or investments.

- Greater comfort with financing: Monthly payments are a normalized part of their financial lives.

- Higher sensitivity to upfront costs: Large out-of-pocket expenses can create hesitation, but these homeowners respond well when projects are framed in terms of manageable monthly payments.

Older Homeowners

- Higher levels of home equity: With more time in their homes, older homeowners typically have greater access to equity, providing flexibility to fund larger or more complex projects.

- Continued caution around liquidity: Despite having available assets, many prefer to preserve cash and avoid significant withdrawals from savings or investment accounts.

- Preference for predictable expenses: This group tends to value stability, favoring clearly defined payment terms and lower-risk financial decisions.

These generational differences directly influence how homeowners evaluate projects, how quickly they make decisions, and what financing structures resonate most. Contractors who recognize and adapt to these nuances are better positioned to meet homeowners where they are and convert more leads into satisfied customers.

What This Means for Contractors Today

Today’s homeowners are evaluating projects through a more complex financial lens. They’re balancing cost, timing, and financial comfort in ways that directly influence how and when they move forward.

These consumer trends are not just market observations; they have direct implications for contractor performance, sales efficiency, and long-term growth.

Contractors who succeed in today’s market are not just selling projects; they are helping homeowners navigate financial decisions with clarity and confidence. That’s where offering flexible payment solutions, clear options, and strong financing partnerships become a competitive advantage.

Adapting to Today’s Homeowner: What to Know Next

Understanding these trends is only the first step. As homeowner expectations continue to evolve, so must the way contractors approach the sale.

In our next blog, we'll break down how to adjust your sales approach with today's homeowner mindset so you can reduce friction, improve close rates, and capture more of the opportunities in front of you.

➡️ Coming soon: How Contractors Can Adapt to Evolving Homeowner Trends

Frequently Asked Questions

Why are homeowners delaying home improvement projects?

Homeowners are delaying home improvement projects due to a combination of rising costs, limited savings, and uncertainty around future income. Even when demand remains strong, financial caution often causes homeowners to postpone non-urgent upgrades or wait for more favorable timing.

Are homeowners still investing in home improvement projects?

Yes. While homeowners are more selective, demand for home improvement remains steady. Projects tied to necessity, maintenance, and energy efficiency especially continue to see consistent investment.

How do homeowners decide whether to move forward with a home improvement project?

Homeowners typically evaluate home improvement decisions by weighing urgency, available savings or financing options, and confidence in their financial situation. Decisions often depend on whether the timing feels financially comfortable and whether the monthly or total cost fits within their household budget.

How do consumer trends affect contractors?

Consumer trends directly impact how homeowners evaluate pricing, timing, and payment options, which can influence project size, sales cycles, and overall close rates.

Should contractors offer financing to homeowners?

Yes. Contractors who offer financing consistently see higher close rates. Financing gives homeowners a practical way to move forward with improvements by spreading costs into monthly payments.

How does inflation impact home improvement demand?

Inflation strains household budgets, making homeowners more hesitant about large expenses. Rising energy prices are also driving demand for efficiency-related projects where homeowners can see a long-term cost payoff.

Supporting Blogs in This Series:

| Supporting Blog | Topic Covered |

|---|---|

| Buy-Now, Pay-Later for Home Improvement | How BNPL is transforming contractor conversations and consumer expectations |

| Energy Prices, Inflation & HVAC Homeowner Decisions | How rising energy costs are driving demand for HVAC upgrades and replacements |

| Generational Home Improvement Trends | How Gen X, Millennials, and Gen Z differ in financial behavior and decision-making |

– Madison Schoppe (Marketing Content Developer)